WeChat Pay AI Card Released? This strategic pivot has been conclusively validated as Tencent officially launches its proprietary payment architecture tailored exclusively for autonomous software agents. On June 17, 2026, WeChat Pay formally rolled out its ‘AI Dedicated Card’ (AI专属卡), establishing a dedicated, main-account-isolated wallet designed to authorize machine-to-machine transactions. For global growth teams, the rapid adoption of this WeChat Pay AI Card triggers an immediate attribution crisis because background-scheduled agentic checkouts execute purchases autonomously without human ad clicks or traditional store redirects.

News & Context Breakdown

Tencent’s Financial Blueprint: Inside the Dedicated Wallet

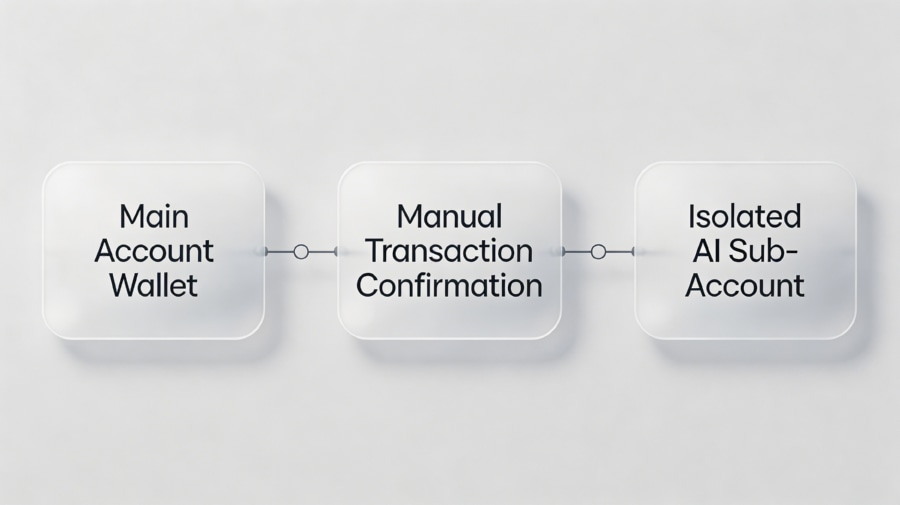

Tencent designed this newly released financial feature to solve a fundamental friction in agentic commerce. Specifically, the architecture introduces a secure, pre-funded sub-account nested inside the standard WeChat Wallet. According to WeChat Pay’s official announcement, the system acts as a digital sandbox wallet.

Tencent Public Relations Director Zhang Jun clarified the underlying logic using a simple analogy. Zhang compared the wallet to a parent giving cash to a child to purchase a specific brand of cigarettes. Consequently, the user remains the ultimate authority.

Additionally, Zhang corrected early consumer misconceptions. Some users initially assumed the product functioned as an AI credit card. In contrast, Zhang explained that users must pre-fund the wallet, making it a strict debit sub-account. Specifically, users top up the card manually to grant the agent its purchasing budget.

The Three Security Walls: Isolation and Authorization Protocols

Crucially, allowing software agents to make financial decisions requires extreme security guardrails. To prevent unauthorized spending, Tencent engineered three distinct security vectors.

- Main Account Isolation: First, the system isolates the agent’s wallet entirely from the user’s primary WeChat Pay bank cards. The agent can only read and use the specific balance allocated to the card.

- Custom Balance Limits: Second, users retain absolute control over the budget. They can transfer funds in or out of the sub-account instantly. This feature ensures that users can claw back allowances immediately if an agent malfunctions.

- Per-Transaction Confirmation: Third, the system enforces manual confirmation. No agent can execute a checkout without the user’s final approval. When an agent initiates a purchase, the user receives a transaction prompt on their mobile device. The purchase fails instantly if the user does not explicitly authorize the transaction.

The WorkBuddy Integration: Observing Local Agentic Checkouts

Meanwhile, Tencent has deployed the first live implementation of this technology within its desktop workspace. Specifically, Mac users running WorkBuddy version 5.1.1 can now experience local agentic checkouts.

Users can invoke the “Meituan Life Assistant” directly through the platform’s assistant directory. For instance, a user can instruct the agent to find a single-person lunch coupon nearby for under 30 yuan. The agent autonomously queries local merchant databases and displays the best options.

Once the user selects a deal, WorkBuddy processes the transaction using the WeChat Pay AI Card. The user completes the payment via a quick confirmation prompt on their mobile device. Consequently, this integration streamlines the purchase, removing the need to manually browse external coupons or type credit card details.

Industry War: Tencent’s Open SDK Strategy vs. Alipay’s Abao

Notably, this release intensifies the rivalry between China’s dominant digital transaction systems. To secure developer adoption, Tencent is opening the SDK to external creators.

Consequently, the payment routing mechanisms must align with WeChat’s official developer guidelines to handle API authentication under high security boundaries. This strategy contrasts with Alipay’s “Abao” agentic framework. Alipay focus on rebuilding its primary super-app interface around a proprietary assistant.

In contrast, WeChat Pay is acting as a modular infrastructure provider. By releasing a developer-friendly payment SDK, Tencent allows external AI agents to integrate payment capabilities easily. This open approach encourages rapid adoption across third-party software platforms. Consequently, it establishes WeChat Pay as the default transaction layer for the autonomous agent economy.

The Routing Gap: Bypasses the App Funnel in Autonomous Transactions

The Transition to Intent-Driven Traffic

The integration of the WeChat Pay AI Card into daily applications marks a major pivot in mobile marketing. Historically, the digital economy relied on explicit, human-centric visual touchpoints. Businesses spent billions optimizing store listings, visual banner ads, and manual shopping carts.

However, when an autonomous agent handles the transaction loop, these visual assets become obsolete. The agent bypasses the traditional user journey completely. It queries product metadata directly, compares pricing matrices, and executes the checkout in the background.

Consequently, we observe a massive shift from active web traffic to intent-driven traffic. Humans no longer browse landing pages or click promotional store redirects. Instead, background software processes make purchasing decisions, rendering traditional advertising channels ineffective.

Bypassing Redirection Mechanics

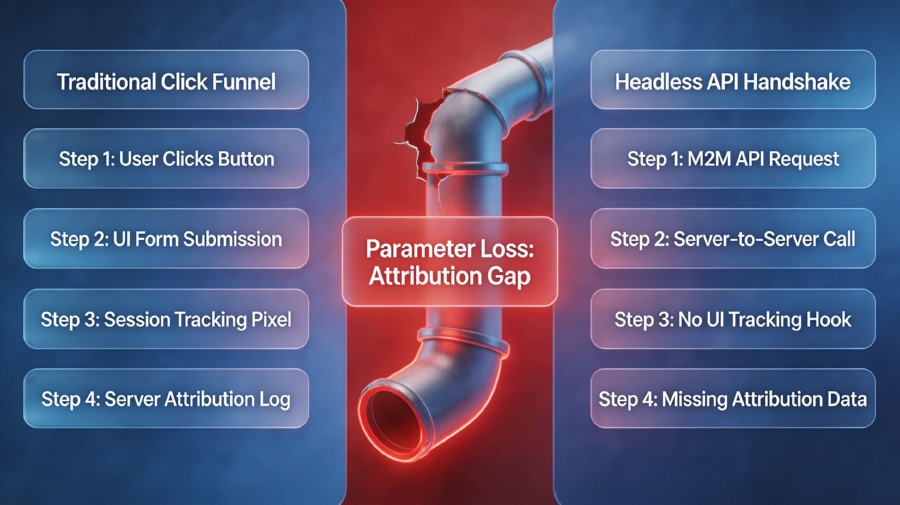

Furthermore, this machine-to-machine checkout model triggers an unprecedented attribution crisis. Legacy mobile tracking depends on cookies, HTTP referrers, and URL query strings. These systems assume the user’s browser executes a series of 302 redirects before reaching the final checkout page.

When an AI agent handles the transaction, these redirection mechanics are completely eliminated. The agent interacts directly with payment gateways via API handshakes. As a result, critical referral parameters and marketing attribution tags are stripped during transit.

Mobile measurement platforms (MMPs) receive empty parameter packages. Consequently, developers lose the ability to trace the origin of the sale. They cannot determine which page, campaign, or automated recommendation drove the conversion.

Technical Reference Architectures & Engineering References

Rebuilding the Parameter Handshake

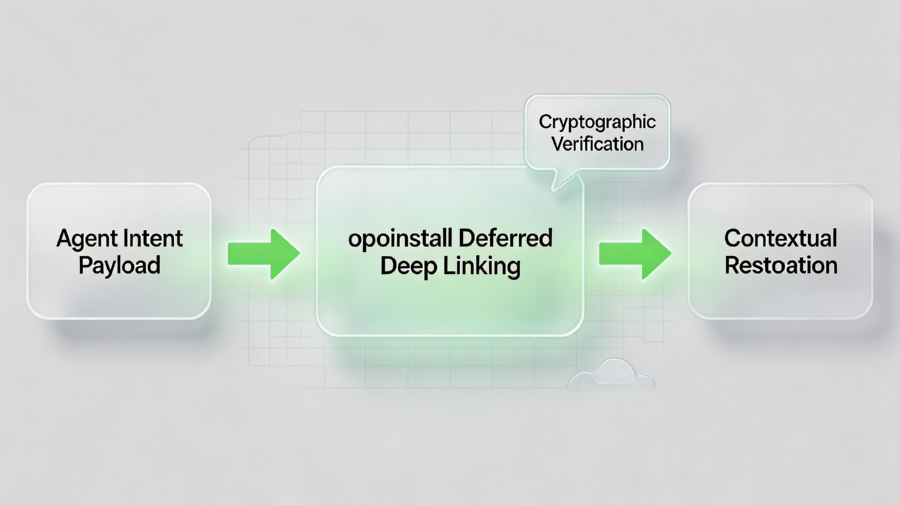

To bridge this semantic routing gap, software architects must deploy secure parameter-preservation frameworks. When an external agent invokes an application, it must transmit a verified payload containing the user’s original intent, referral parameters, and security tokens.

Crucially, developers can establish a resilient solution using the Deferred Deep Linking framework. This system ensures that dynamic payload parameters survive background installation loops. Even if the device lacks the native application, the contextual restoration infrastructure preserves the intent payload, passing it securely to the app upon first launch.

Cryptographic Verification for Machine-to-Machine Transactions

Additionally, securing these automated transactions requires strict cryptographic handshakes. Because background agents operate without visual human supervision, malicious scripts can attempt to spoof transaction requests.

To prevent this, every deep link routing request must carry a verifiable cryptographic signature. The application must validate this signature against public developer registries before executing any action.

Enforcing a secure Deferred Deep Linking framework allows development teams to execute these validations automatically. This process protects the application sandbox from fraudulent installations and secures the transaction pipeline against ad fraud.

Industry Forward-looking Note: Regarding cross-device parameter passing for autonomous intent traffic, opoinstall’s tech lab is currently conducting joint exploratory research with leading enterprise App partners.

Impact on Dev & Growth Teams

For Developers and System Architects

Integrating a native WeChat Pay AI Card into the application architecture requires a major shift in development practices. Engineers must transition from designing traditional visual navigation paths to constructing detailed App Intents. These intents allow system-level agents to read app structures and query data programmatically.

Furthermore, developers must implement strict signature verification to validate all incoming deep link payloads. This validation prevents rogue agents from executing local sandbox escapes or triggering fraudulent purchases. Architects must also configure unified multi-platform ID systems to track the user journey across iOS, Android, and HarmonyOS NEXT.

For Product and Growth Managers

Meanwhile, product and marketing leads must redefine their growth metrics. In an agentic environment, traditional KPI metrics like page views, bounce rates, and session lengths lose their value.

Instead, growth leads must optimize for “Intent Capture Rates”. They must ensure their application provides highly structured, machine-readable metadata that agents can parse easily.

Additionally, teams must deploy advanced anti-fraud filters to identify and block automated script-based downloads. This protection ensures that acquisition budgets are spent on real user growth rather than inflated, machine-generated traffic.

Frequently Asked Questions (FAQ)

How does the WeChat Pay AI Card prevent unauthorized spending?

Specifically, the system relies on strict account isolation. The card operates with an independent balance separated from the user’s primary bank cards. Users must manually top up the card. Furthermore, the system requires mobile-side confirmation for every purchase, ensuring the user retains ultimate control.

Why does agent-driven purchasing trigger an attribution crisis?

Notably, background agents bypass the traditional visual browser funnel completely. Because they query APIs and execute checkouts programmatically without clicking ad banners or viewing store redirect pages, traditional tracking parameters are lost. This parameters loss prevents developers from identifying the marketing source of the transaction.

Can traditional mobile tracking tools adapt to machine-to-machine transactions?

No, legacy tracking systems depend on human-centric interactions like clicks and browser cookies. To track autonomous agent checkouts, developers must transition to parameter-rich, deep linking frameworks. These systems carry cryptographic intent tokens directly from the agent’s query into the native app environment.

Industry Observations

Ultimately, the traditional click-based economy is facing a rapid decline. As payment networks and device operating systems transition to autonomous agentic architectures, the value of software is shifting to the underlying routing layer.

Consequently, building robust, parameter-secure deep linking backbones is no longer a luxury. It is a baseline operational requirement. By preparing your application architecture for the agentic economy today, you ensure your software remains accessible, verified, and profitable in the post-screen era.